The Prediction Markets Preemption Question Reaches New York

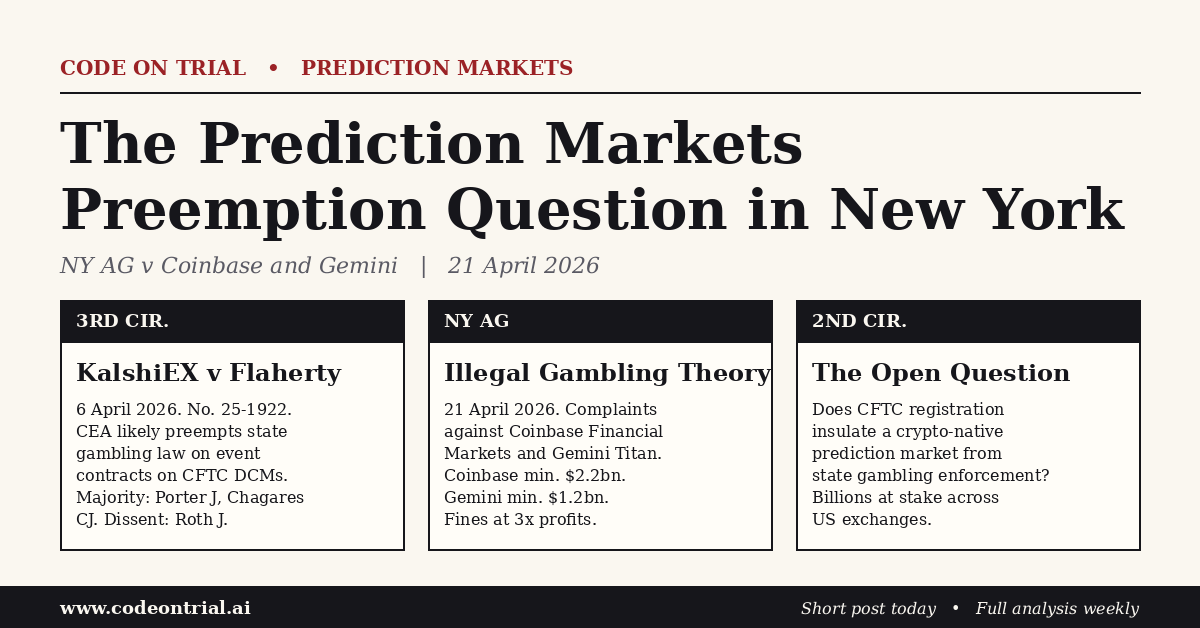

New York Attorney General Letitia James commenced proceedings on 21 April 2026 against Coinbase Financial Markets, Inc. and Gemini Titan, LLC over their prediction market products, seeking illegal-profit disgorgement, restitution, civil fines equal to three times the operators’ profits and reported minimum damages of $2.2bn from Coinbase and $1.2bn from Gemini.1

The complaints were filed fifteen days after the Third Circuit held in KalshiEX LLC v Flaherty, No. 25-1922, that the Commodity Exchange Act likely preempts state gambling enforcement against sports-related event contracts traded on CFTC-licensed Designated Contract Markets.2 The alignment of CFTC registration, state gambling theory and federal circuit geography now determines the litigation risk for every exchange offering event contracts.

The preemption architecture

Judge David Porter’s majority opinion in Kalshi, joined by Chief Judge Michael Chagares and affirming the District of New Jersey’s preliminary injunction against the New Jersey Division of Gaming Enforcement, rested on two bases. Field preemption followed from the CFTC’s exclusive jurisdiction over swaps, including sports-related event contracts, traded on DCMs. Conflict preemption followed from the statutory purpose of avoiding the state-by-state regulatory patchwork that the Commodity Exchange Act was designed to displace.3 Judge Jane Richards Roth’s dissent, treating Kalshi’s contracts as sports betting in structural fact, keeps the doctrinal question live for state regulators.

Gemini Titan received its DCM designation on 10 December 2025. Coinbase Derivatives, LLC, the group’s DCM affiliate acquired via FairX, has held DCM status since 23 November 2020. Coinbase Financial Markets, Inc., the entity James has sued, is registered as an FCM. On 2 April 2026, the CFTC commenced federal proceedings against Arizona, Connecticut and Illinois, asserting exclusive jurisdiction over event contracts traded on registered DCMs. On 8 April, a federal court in Arizona granted preliminary injunctive and temporary restraining relief on the same theory. By 21 April, the preemption argument had been accepted or endorsed by several federal courts, including the Third Circuit and, most recently, the District of Arizona.4

The Second Circuit question

New York sits in the Second Circuit, which has not ruled on CEA preemption in the event-contract context. The Third Circuit opinion is persuasive authority, not binding authority. Its reasoning nevertheless transports without much strain to event contracts traded on CFTC-licensed DCMs. The Second Circuit has previously recognised broad CEA preemption in the futures context, and section 2(a)(1)(A) of the Commodity Exchange Act contains the exclusive-jurisdiction language on which the Kalshi majority relied.5

The entity split matters to New York’s pleading design. Coinbase Financial Markets is an FCM. Coinbase Derivatives is the DCM and is not a named defendant. The preemption defence, which runs through DCM registration under section 2(a)(1)(A), therefore reaches the DCM directly but reaches Coinbase Financial Markets only to the extent that the event contracts at issue are allocated to, or transacted through, the DCM affiliate. Gemini Titan carries its DCM registration in its own name and has the cleaner preemption posture of the two defendants.

The litigation design tells us something about the target. New York is attempting to build a doctrinal record in a circuit not yet bound by Kalshi, while Kalshi itself, which James has not named, remains the structurally strongest preemption defendant.

Practitioner implications

For crypto-native exchanges offering event contracts, three questions now follow. First, whether product migration from FCM-facing to DCM-facing entity structures is required for full preemption coverage against state gambling enforcement. Second, whether the New York actions should be removed to federal court and consolidated, coordinated or otherwise sequenced with federal proceedings raising the same preemption issue. Third, whether state attorneys general will treat CFTC registration as a negotiating chip rather than a jurisdictional bar.

The structural issue is adjacent to the federalism problem Justice Alito identified in Murphy v National Collegiate Athletic Association: where Congress regulates directly and does so with sufficient clarity, preemption turns on statutory text rather than state gaming authorities’ characterisation of the product.6 The Third Circuit has resolved the question at preliminary-injunction stage for sports-related event contracts traded on CFTC-licensed DCMs. The Second Circuit, sooner rather than later, will be asked whether to follow. Whether it does, and on what reasoning, will shape the next generation of prediction-market litigation and the asset class it surrounds.

1 Office of the NY Attorney General press release, Attorney General James Sues Coinbase and Gemini for Running Illegal Gambling Platforms in New York (21 April 2026). Reuters, CoinDesk, CNBC, American Banker and CBS New York (21 April 2026). The proceedings were commenced in New York state court in Manhattan.

2 KalshiEX LLC v Flaherty, No. 25-1922 (3d Cir., decided 6 April 2026). Slip opinion via Justia. Skadden, Third Circuit Affirms Kalshi’s Preliminary Injunction (April 2026). Paul, Weiss, A Divided Third Circuit Holds That the CFTC Has Exclusive Jurisdiction Over Sports-Related Event Contracts (April 2026).

3 KalshiEX LLC v Flaherty, slip opinion. For earlier federal decisions considering the preemption theory, see the Kalshi majority’s citations to M.D. Tenn. (19 February 2026), N.D. Cal. (10 November 2025) and D.N.J. (28 April 2025).

4 Gemini Investor Relations release, Gemini Receives US License for Prediction Markets (10 December 2025). CFTC DCM Registry entries for Gemini Titan, LLC and Coinbase Derivatives, LLC (legacy LMX Labs / FairX, designated 23 November 2020). CFTC release, 2 April 2026, multi-state proceedings against Arizona, Connecticut and Illinois. District of Arizona, Preliminary Injunction and Temporary Restraining Order (8 April 2026), available via the CFTC case portal.

5 Commodity Exchange Act, section 2(a)(1)(A). Specific Second Circuit CEA preemption authority to be added by the author on publication.

6 Murphy v National Collegiate Athletic Association, 584 US 453 (2018). The Court struck down the Professional and Amateur Sports Protection Act on anti-commandeering grounds and discussed preemption principles in the course of doing so. Murphy does not itself resolve the CEA / event-contract preemption question.